Our policies are available exclusively through UK brokers

Frequently asked questions

If you can't find the answer you're looking for? Contact our team who will be happy to help.

About ERS

Our accreditations and policies including information on the modern slavery act.

ARC

Find links to ARC here.

Broker marketing

Raise your profile with bespoke marketing material from our list of preferred suppliers.

Claims

Everything you need to know about making a claim, from when to report an incident to paying policy excess.

Complaints

We aim to provide a first class service, but if anything ever goes wrong you’ll find how to make a complaint here.

Cover Note and Green Card portal

ERS eTrade

FCA Fair Pricing

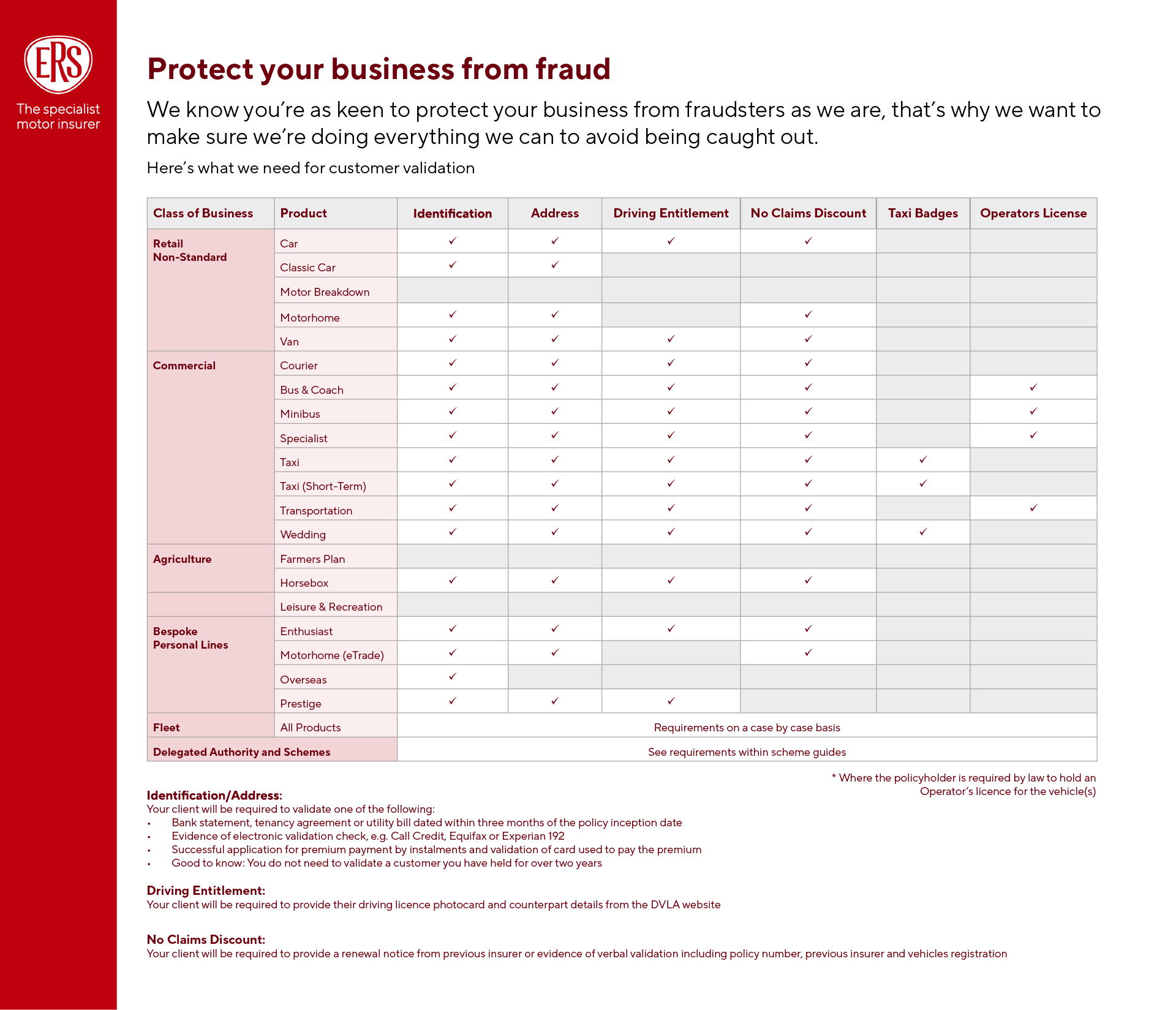

Fraud

We treat fraud extremely seriously. Find out more about our policy and initiatives to prevent and mitigate fraud.

If you suspect fraud then please contact our dedicated hotline on 03300 535 891. All calls will be treated in the strictest confidence.

ERS has a zero tolerance to claims fraud because it can negatively affect innocent policyholders in two ways:

- The Association of British Insurers believes that it adds £50 to the cost of motor insurance premiums.

- Criminals may seek to manoeuvre innocent motorists into induced accidents in order to benefit from claims.

If you suspect fraud then please contact our dedicated hotline on

03300 535 891. All calls will be treated in the strictest confidence.

It is important that your insurance policy is based on the correct information.

Providing incorrect or false details, or failing to disclose information when requested, could render your insurance policy as 'null and void' or cancelled.

To ensure we sell the correct cover, the following are details which may be checked by ERS, or your broker on our behalf:

- Your claims history

- Your identity

- Your address

- The validity of any debit or credit card used to purchase your policy – to ensure that stolen and cloned cards are not used

- Your No Claims Bonus entitlement

- The ownership of your vehicle

- Any motoring convictions you have

- Your taxi license - if applicable

- That approved security devices are fitted - where required under our policy terms Whether you or any named drivers have had previous insurance cancelled or declared void for fraud reasons

To help prevent fraud, we work with the following organisations:

- Insurance Fraud Bureau - the IFB are a 'not for profit' organisation focussed on detecting and preventing organised insurance fraud.

- Insurance Fraud Enforcement Department - the IFED are a dedicated team at City of London Police, targeting the investigation of insurance fraud at all levels and from all sectors.

Leaving the EU & Green Cards

Motor Insurance Bureau (MIB)

Policy docs, IPIDs and Key Facts

All the paperwork you ever need to put together an ERS policy for a customer can now be found in our For Brokers pages, or on the relevant product page.

Soft Credit Searches

Why it's important to inform your clients about soft credit searches

As a broker, it’s important to let clients know that a soft credit search may be carried out during the motor insurance quote process.

These checks help verify identity, confirm details, and support fraud prevention. They won’t affect a client’s credit score and are only visible to them.

Insurers like IQUW Group (parent company of ERS) may run these checks even if a quote doesn’t go ahead. Being upfront helps manage expectations and reinforces trust in the process.

About ERS (Policyholders)

COVID-19 (Policyholder)

Claims (Policyholder)

Complaints (Policyholder)

Fraud

We treat fraud extremely seriously. Find out more about our policy and initiatives to prevent and mitigate fraud.

If you suspect fraud then please contact our dedicated hotline on 03300 535 891. All calls will be treated in the strictest confidence.

ERS has a zero tolerance to claims fraud because it can negatively affect innocent policyholders in two ways:

- The Association of British Insurers believes that it adds £50 to the cost of motor insurance premiums.

- Criminals may seek to manoeuvre innocent motorists into induced accidents in order to benefit from claims.

If you suspect fraud then please contact our dedicated hotline on

03300 535 891. All calls will be treated in the strictest confidence.

It is important that your insurance policy is based on the correct information.

Providing incorrect or false details, or failing to disclose information when requested, could render your insurance policy as 'null and void' or cancelled.

To ensure we sell the correct cover, the following are details which may be checked by ERS, or your broker on our behalf:

- Your claims history

- Your identity

- Your address

- The validity of any debit or credit card used to purchase your policy – to ensure that stolen and cloned cards are not used

- Your No Claims Bonus entitlement

- The ownership of your vehicle

- Any motoring convictions you have

- Your taxi license - if applicable

- That approved security devices are fitted - where required under our policy terms Whether you or any named drivers have had previous insurance cancelled or declared void for fraud reasons

To help prevent fraud, we work with the following organisations:

- Insurance Fraud Bureau - the IFB are a 'not for profit' organisation focussed on detecting and preventing organised insurance fraud.

- Insurance Fraud Enforcement Department - the IFED are a dedicated team at City of London Police, targeting the investigation of insurance fraud at all levels and from all sectors.

Leaving the EU & Green Cards (Policyholder)

Motor Insurance Bureau (MIB)

Windscreen Repairs

Soft Credit Searches

Understanding soft credit searches during the quote process

When you request a motor insurance quote, insurers may perform a soft credit search to verify your identity and information. This doesn’t affect your credit score and is only visible to you. Companies like IQUW, ERS’s parent company, may conduct these checks even if you don’t take up the quote. Your data is handled securely and in line with data protection laws. Please speak to your broker if you have any questions or concerns.